The NAX Index – July 2026

Read More

Published: July 13, 2026

Last Updated: July 16, 2026

Higher rates are being driven more by supply-and-demand imbalance than by diesel prices.

North American freight demand is up modestly, but reduced carrier capacity is having the biggest impact in pushing rates higher.

Constrained Capacity

The reduction in available trucking capacity is becoming increasingly evident across the freight market. Higher tender rejection rates mean shippers are relying more on secondary carriers and the spot market to move freight. With fewer capacity options available, carriers have greater leverage to negotiate higher rates.

Demand Continues to Improve

Economic indicators and freight volumes indicate that year-over-year shipping volumes are starting to increase. U.S. manufacturing indicators have turned positive in 2026 after years of contraction.

Freight Rates Remain Elevated

While fuel continues to increase transportation costs, it is not the primary driver of higher freight rates. Instead, tighter capacity is allowing carriers to be more selective, prioritizing higher-margin freight and keeping overall rates elevated.

Cross-Mode Pressure

As truckload capacity tightens, the effects are also being felt across other modes of freight. Shippers who have flexibility to shift between transportation modes are finding savings through intermodal. LTL consolidation, pulling inventory forward, and warehouse repositioning are also strategies to consider.

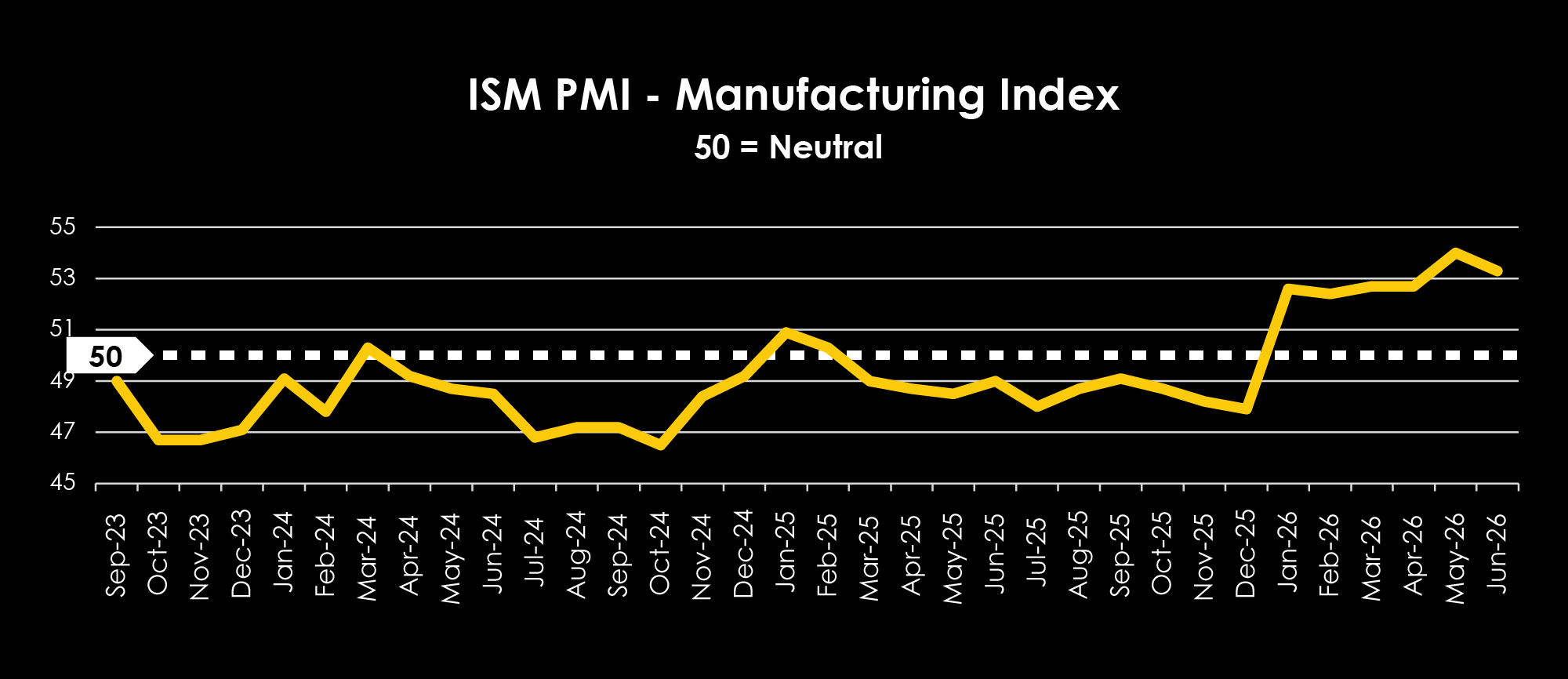

Manufacturing remained in expansion during Q2, while freight transportation remained expensive.

The Transportation Prices Index from the Logistics Managers’ Index (LMI) remained exceptionally elevated throughout Q2, rising to 96.0 in May before easing to 92.4 in June. At the same time, the Transportation Capacity Index fell to 30.8 in June, indicating continued contraction in available capacity. Together, these trends suggest that higher freight rates are being driven by constrained capacity rather than temporary market fluctuations.

Source: LMI

U.S. manufacturing remained in growth mode for the sixth consecutive month. Manufacturing activity and inventory levels both increased during Q2, supporting stronger freight demand. The increase in inventories may also indicate that companies are bringing in goods earlier to help manage tightening capacity and rising transportation costs.

Source: PMI

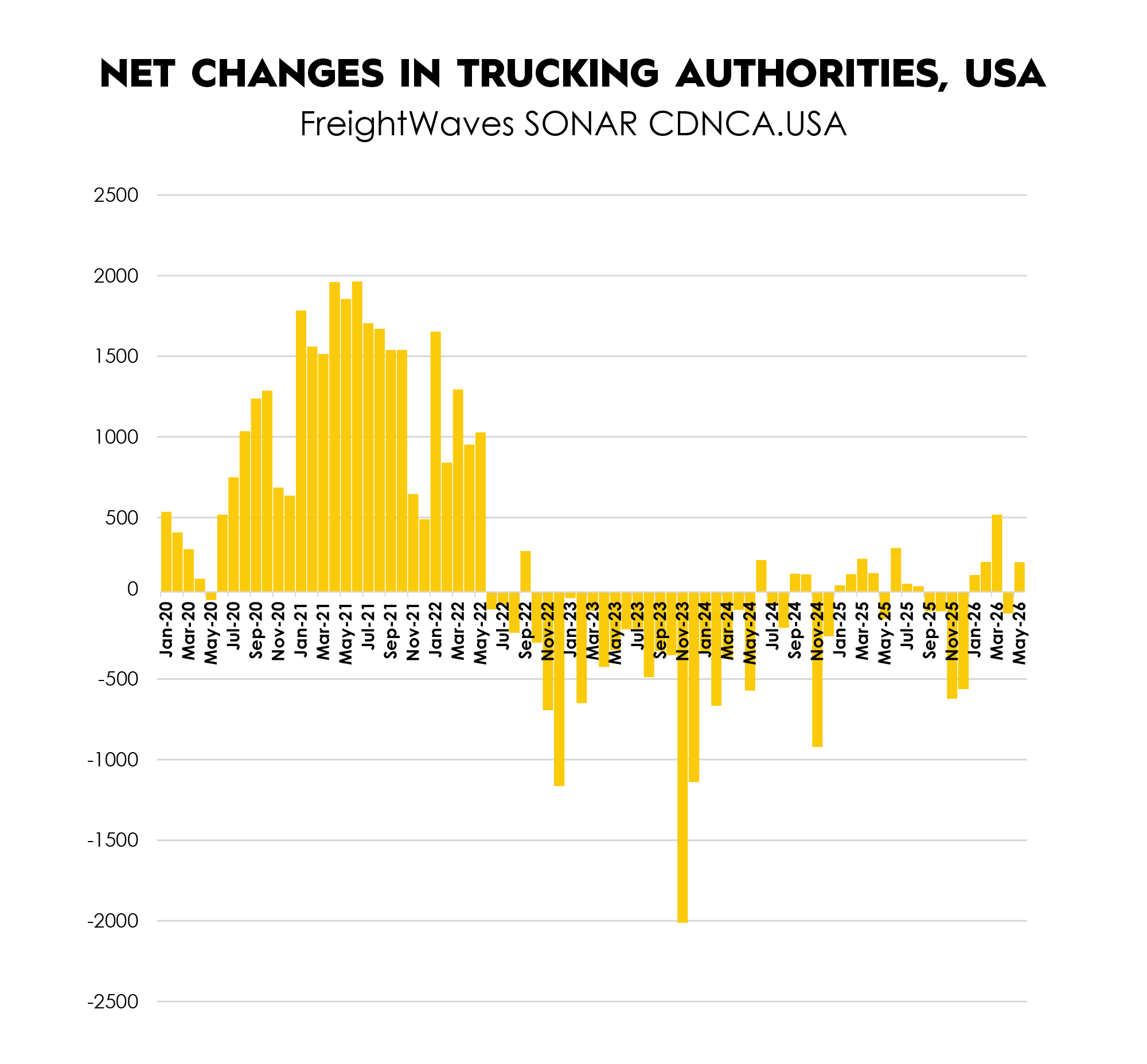

New trucking capacity is entering the market slowly, leaving the market more sensitive to increases in shipping demand.

The number of new trucking companies entering the market improved earlier this year, but the recovery has been inconsistent. After a stronger March, the number of new carriers declined in April before recovering slightly in May.

While fewer trucking companies are leaving the market than from 2022 to 2024, new companies are not entering quickly enough to rebalance demand. As a result, the supply of available trucks remains limited.

Until a larger inflow of drivers and equipment enters the market, rates will remain elevated as demand outpaces supply.

Source: FreightWaves SONAR July 8, 2026

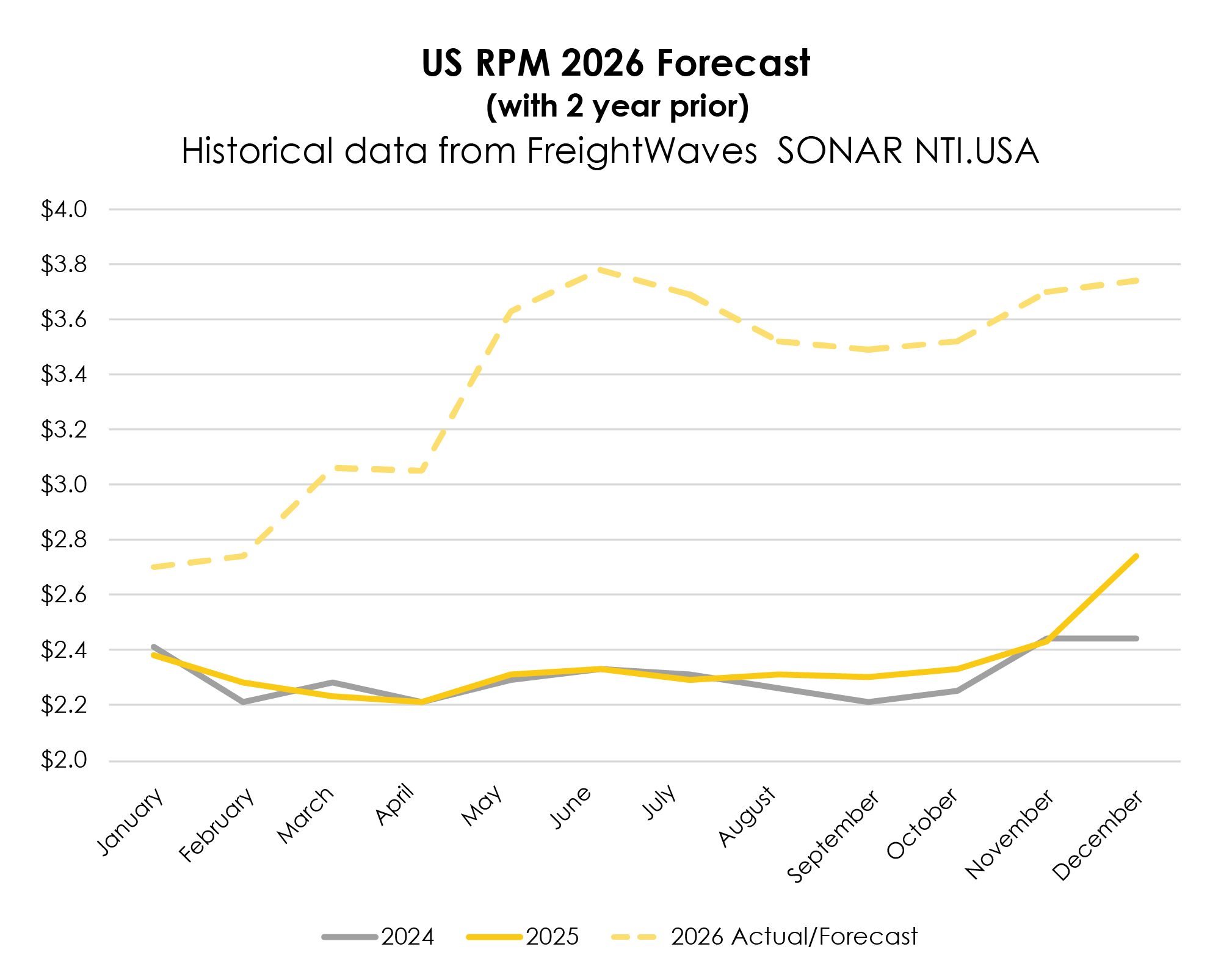

Fuel is accelerating rate increases, but underlying supply-demand dynamics remain the primary driver of inflation.

Source: FreightWaves SONAR July 8, 2026

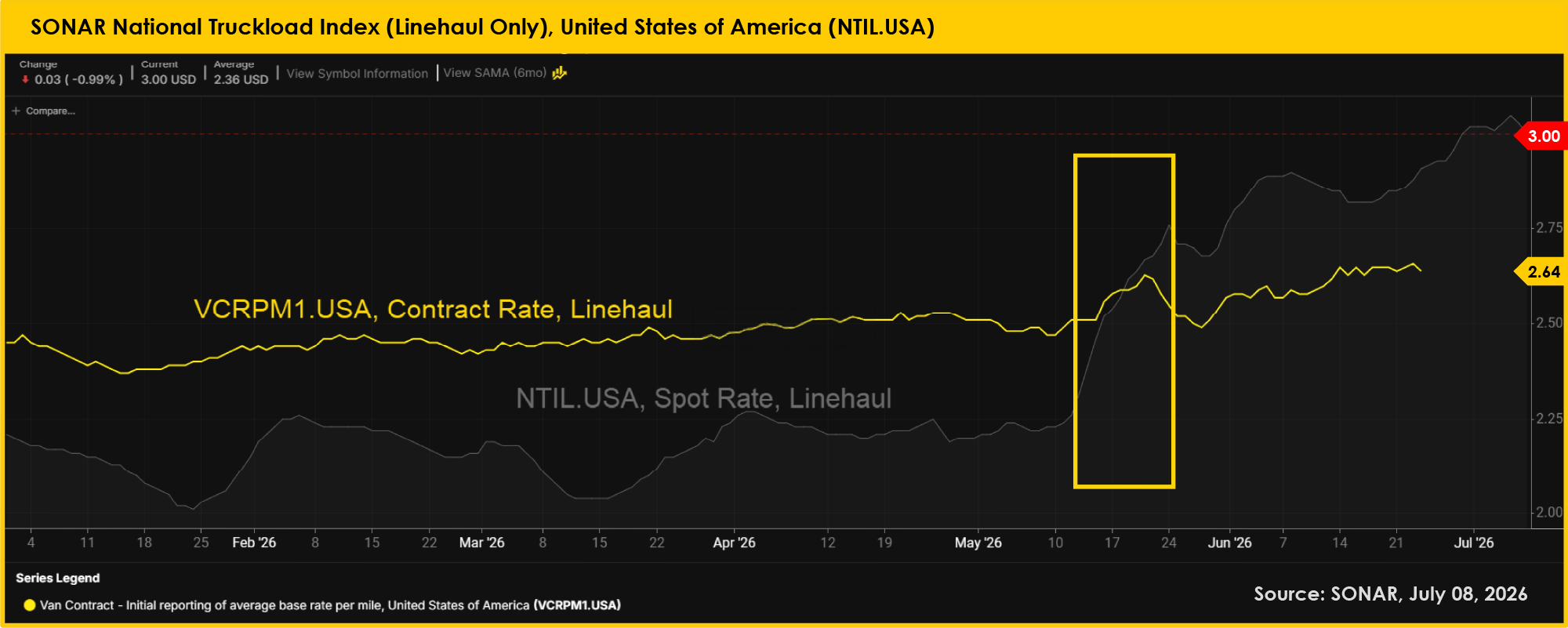

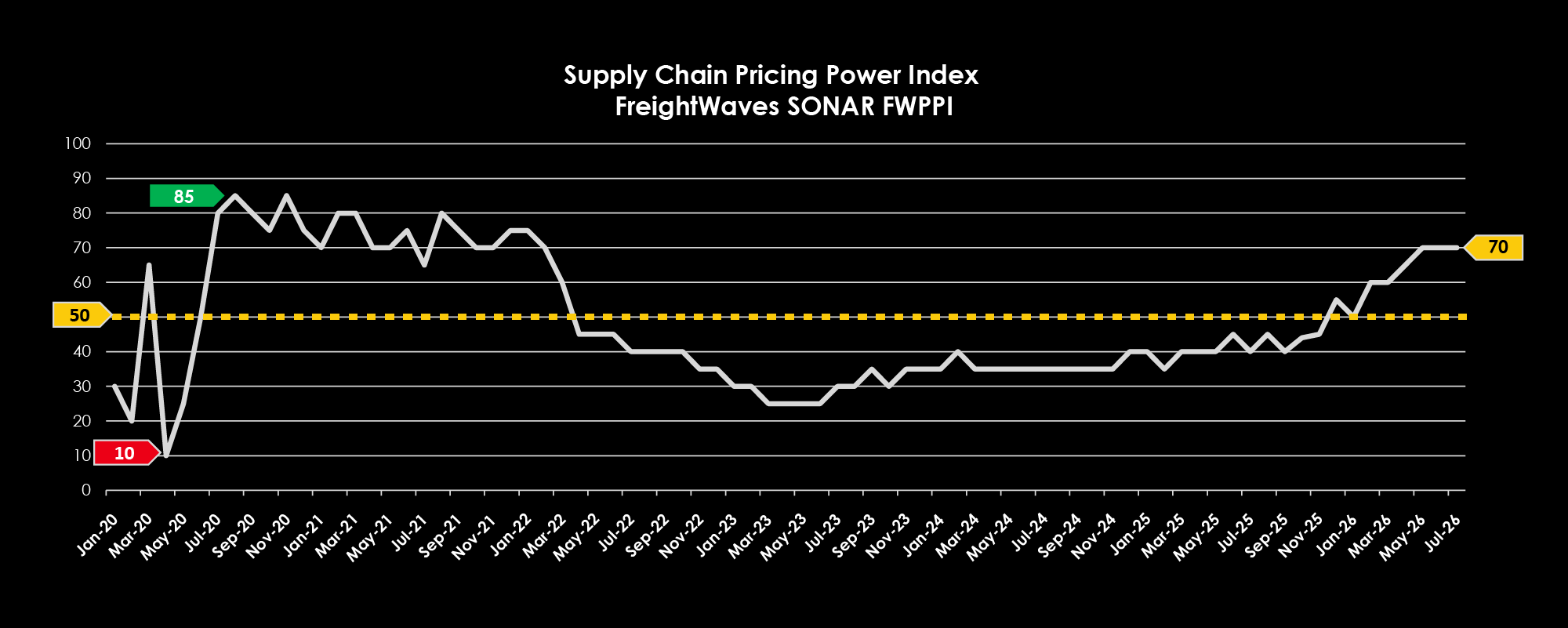

Not seen since the freight market during the COVID pandemic, a contract/spot inversion often drives up contract rates quickly.

The FreightWaves SONAR Supply Chain Pricing Power Index shows that negotiating power has shifted meaningfully back toward carriers. After remaining below the neutral 50 mark for most of 2023 and 2024, the index has climbed steadily and is now sitting around 70, indicating that carriers currently hold more pricing power than shippers.

This shift reflects a tighter freight environment, with higher rejection rates, elevated spot rates, and reduced capacity flexibility giving carriers more leverage in both spot pricing and contract rebids. While the market is still not at the extreme carrier-favorable levels seen during the COVID-era cycle, the balance has clearly moved away from the shipper-favorable conditions of the past two years. Looking ahead, the market is likely to remain carrier-favorable in the near term unless capacity returns more quickly or freight demand softens materially.

Source: FreightWaves Sonar July 10, 2026

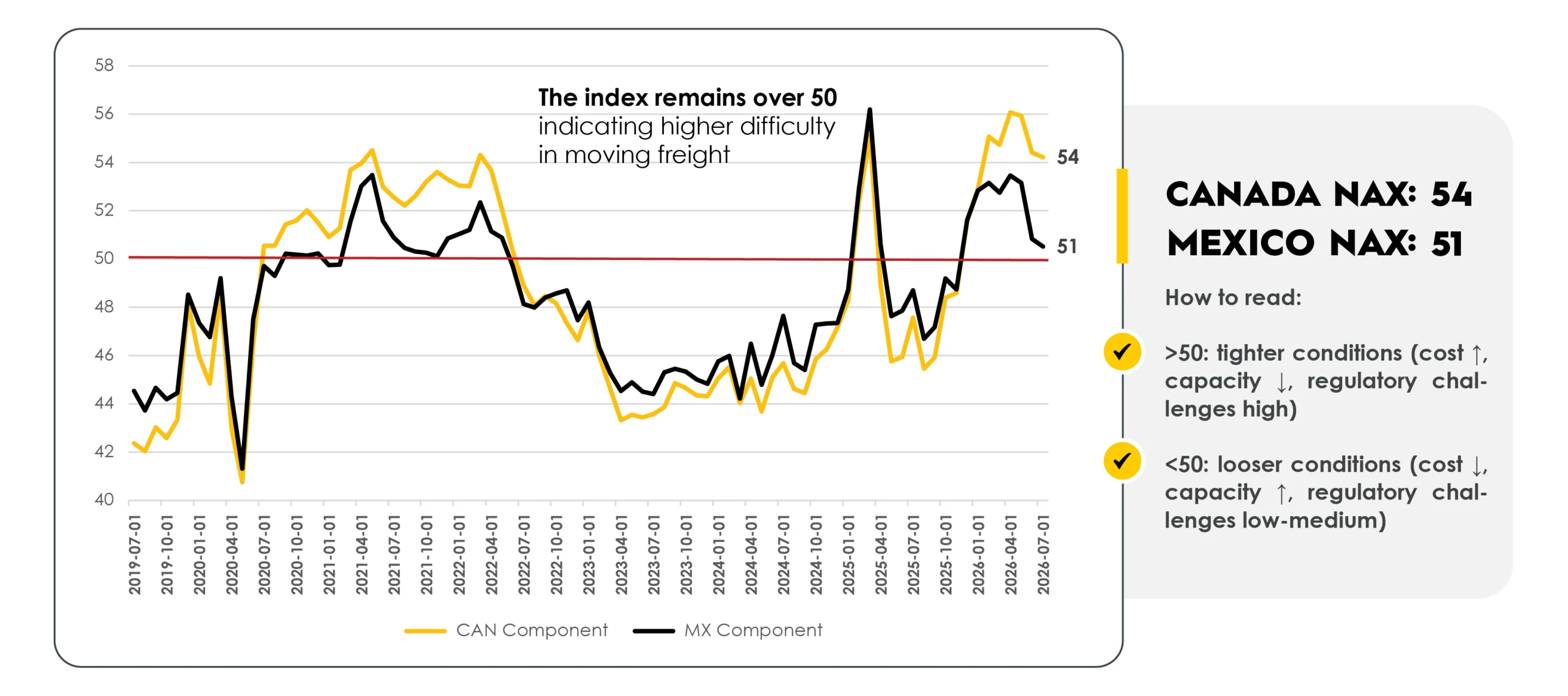

Your Barometer For Ease of North American Cross-Border Freight

Capacity continues to keep the market challenging, while demand and costs remain relatively balanced.

Source: NAX, July 2026

Dry van rates are expected to remain elevated through 2026, driven primarily by tight capacity. Shippers will face challenges locking in long-term capacity until freight demand and supply are better aligned.

LTL freight rates are expected to remain stable, with potential increases later in 2026. Carriers still have available capacity, but they are maintaining pricing discipline. Stronger shipping demand and freight shifting from full truckload to LTL are also increasing pressure on parts of the network. GRIs could increase rates further in Q3 and Q4.

Flatbed markets are tightening rapidly due to construction, infrastructure, and industrial demand. Expect continued upward pressure on rates through peak season.

Refrigerated capacity tightened as seasonal shipping demand increased. Rates are not expected to drop significantly through the end of the produce season, with some potential relief in the fall before protect-from-freeze demand increases.

Intermodal shipping volumes are expected to increase by more than 20% compared to last year as more shippers look for alternatives to a tightening truckload market. Available intermodal capacity is becoming limited in some origin markets. Shippers who book early will have the best chance of securing capacity and avoiding disruptions.

Drayage demand accelerated earlier than expected as tariff uncertainty caused shippers to pull-forward freight. The market is seeing localized congestion and tighter operating conditions, making early planning and flexible capacity critical for shippers. Expect continued volatility through next quarter as peak season develops.

Outbound freight rates have eased in recent weeks as diesel prices have declined, while inbound rates have remained stable. Some relief has emerged in the Southeast and California as the produce shipping season shifts. Expect stabilization in Q3 and Q4, with opportunities to secure a mix of both competitive spot rates balanced with higher rates in high-demand timeframes.

Demand for warehouse space is increasing as shippers build inventory ahead of possible tariffs and the peak shipping season. With many facilities already operating near capacity, available space is becoming harder to find and more expensive. If inventory levels continue to rise, more companies may need to lease additional space, which could keep warehouse costs elevated in major markets.

3 Planning Scenarios for the Remainder of 2026

1. Rates remain high for the rest of the year

Rates are currently hovering around multi-year highs as shipping capacity is unable to meet freight demand. We can expect the higher rates from this imbalance to remain in place for the remainder of 2026. Additional capacity is slowly coming online, but year-over-year freight demand is also increasing. With contract and spot rates inverted, contract rates will continue to increase even as spot rates plateau. Do not expect meaningful rate reductions in 2026, with contract rates likely increasing until the spot/contract inversion concludes.

2. Economic slowdown pushes down demand (and rates)

As inflation flows through the economy, consumer spending and manufacturing could slow. This would decrease freight demand, which would align it closer with reduced freight capacity. This would bring freight rates down as part of an overall economic slowdown. Peak season would be muted, although 2025 rates are still unlikely.

3. Fuel pushes rates higher

Renewed conflicts in the Middle East and depleted oil reserves could push the cost of diesel back up to all-time highs, with that cost increase flowing through to freight rates. With carrier capacity already reduced, this could push rates up further – not only spot, but also contract rates via fuel tables. This could increase freight costs even above all-time records seen in early July.

Planning Guidance:

The most likely scenario is for spot rates to remain around their current range for the remainder of 2026, and contract rates to continue rising until they are no longer below spot. An economic slowdown could push rates lower, and higher diesel rates could have the opposite effect. Budgeting should anticipate contract rate inflation throughout the rest of the year.

Freight capacity will remain tight for the remainder of 2026

Do not assume freight rates will return to 2025 levels anytime soon. Use current transportation costs as the starting point for your budget, and plan for higher costs if you rely on the spot market, expedited shipping, short-haul shipments, or high-demand lanes.

Book transportation on your most important shipping lanes before demand increases. Committing freight early, reviewing rates more frequently, and working with multiple trusted carriers can help reduce the need for higher-priced spot shipments.

Look for opportunities to be flexible with how and when freight moves. Using intermodal when transit times allow, consolidating LTL shipments, and planning shipments further in advance can help reduce transportation costs and lower the risk of delays.