The NAX Index – July 2026

Read More

Published: March 31, 2026

Last Updated: June 19, 2026

Market Overview

What This Means for the Market

Current conditions point to a cooling period following Roadcheck and Memorial Day pressure, not a full market reset. While some indicators have softened, underlying cost pressure remains active and has not shown meaningful signs of relief.

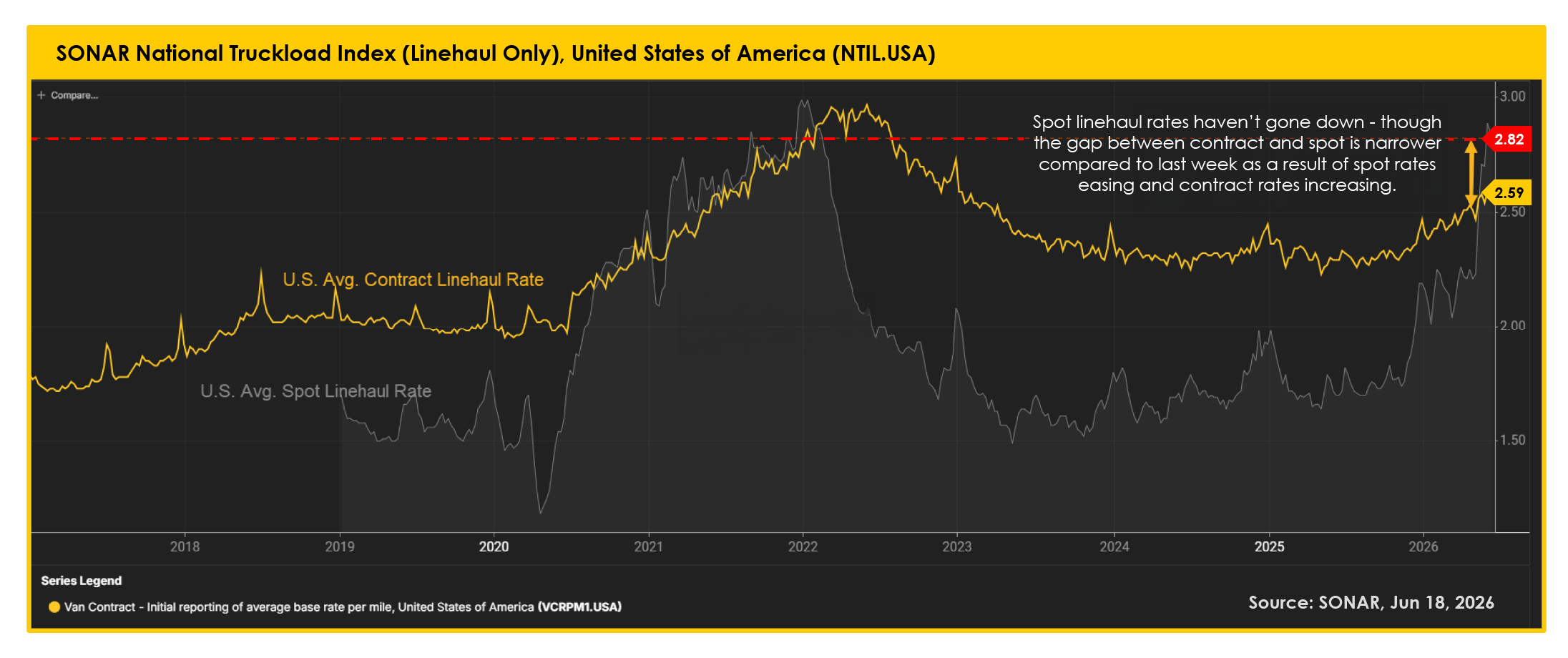

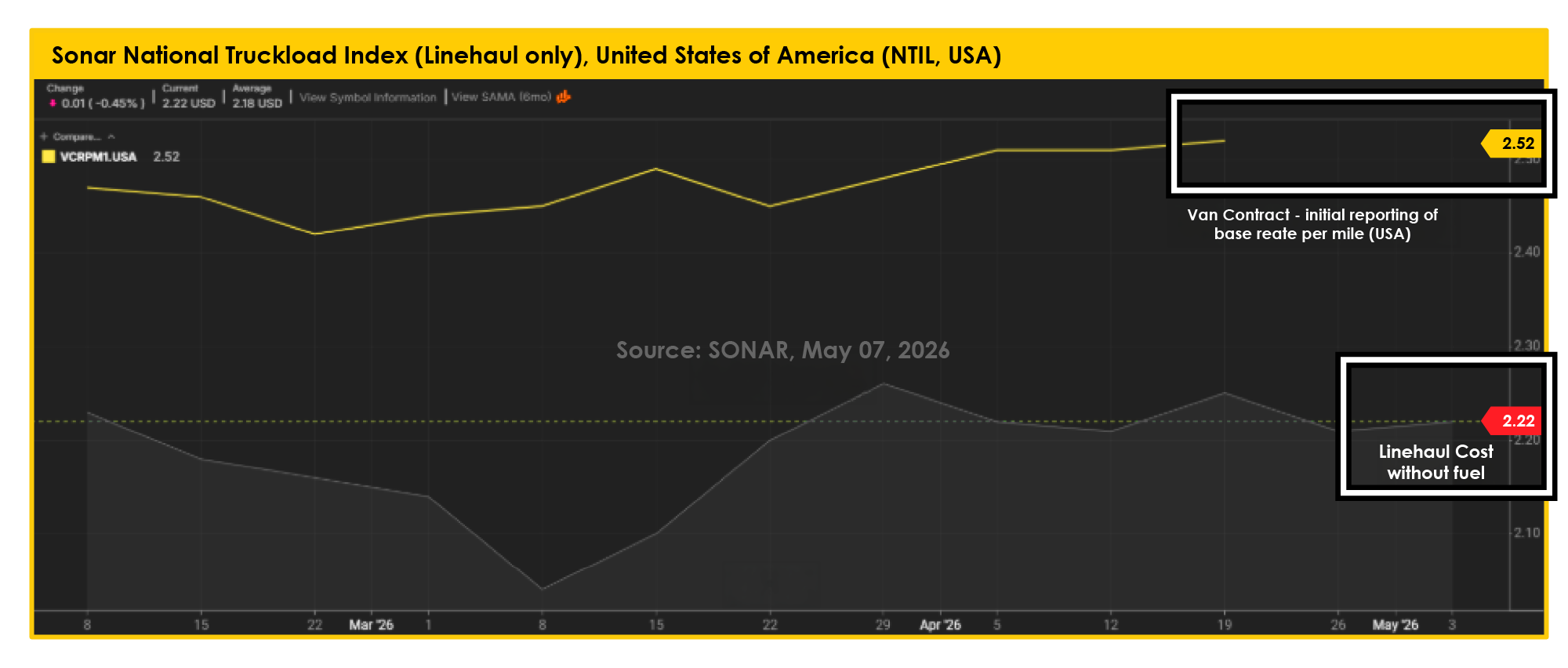

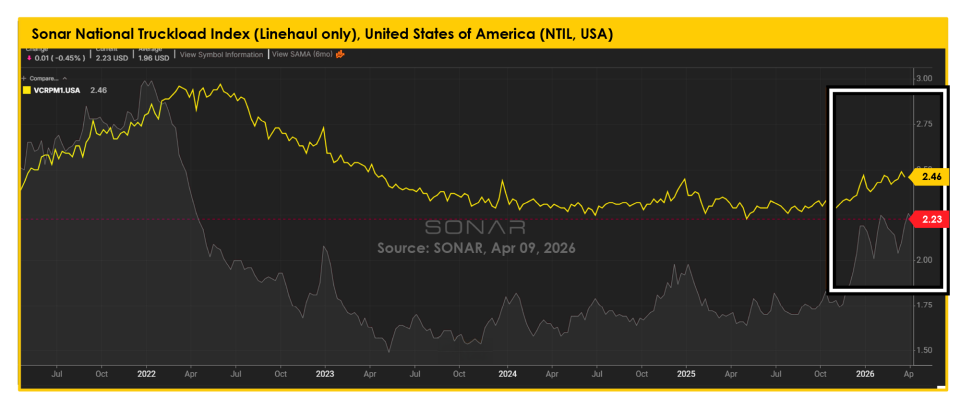

Linehaul spot rates continue to run above contract rates, meaning last-minute freight is still priced higher than planned contract freight. The gap between spot and contract rates has narrowed, but primarily because spot rates eased while contract rates moved higher. This suggests contract pricing is beginning to catch up to the elevated spot market rather than the market fully resetting.

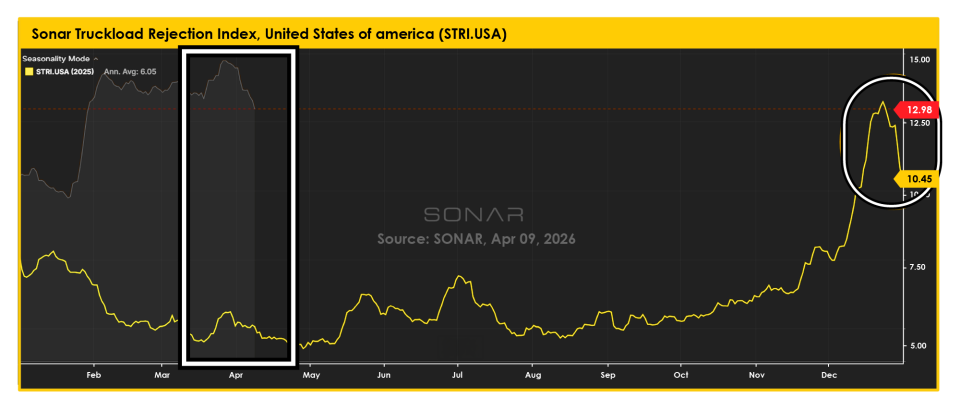

Tender rejections remain elevated. Even with the slight dip, rejection rates near 17% indicate that carriers continue to hold leverage and are not accepting every contracted load.

Volumes are also still holding above last year. Even with a modest decline from two weeks ago, demand has not fallen enough to meaningfully loosen capacity.

For shippers, the main takeaway is that cost pressure remains active. The market may not be climbing as quickly as it was earlier in June, but it is also not returning to normal yet.

Areas to Watch

Strategic Considerations

Market Overview

What This Means for the Market

The market remains under pressure from a combination of regulatory challenges, broader economic uncertainty, and continued capacity constraints.

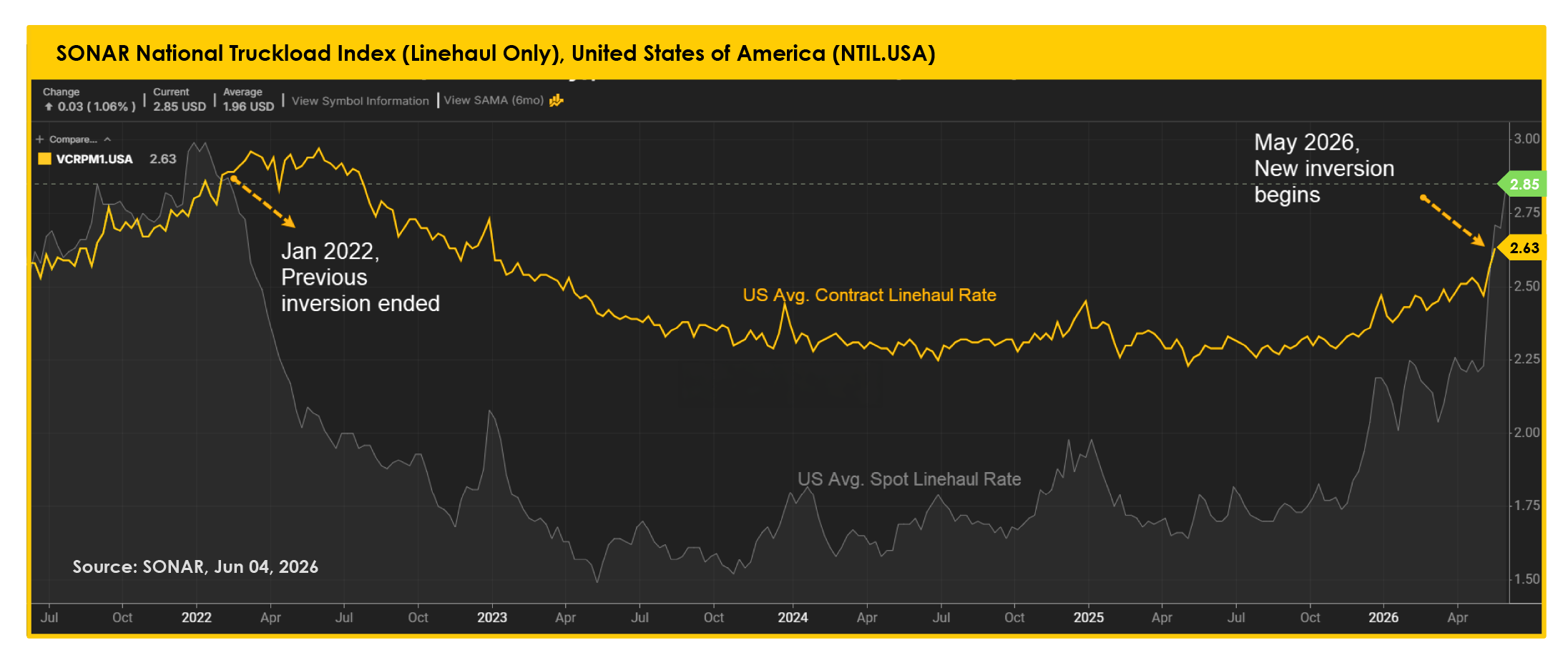

One of the strongest indicators of current market conditions is that linehaul spot rates remain above contract rates. This is a pattern not seen since the COVID freight cycle and suggests that capacity remains tighter than many expected following the holiday period.

Last-minute freight continues to cost more than planned contract freight. When shippers need coverage outside of their contracted carrier network, they are still paying a premium, reflecting ongoing pressure in the spot market.

Tender rejections provide another important signal. With rejection rates above 17%, carriers are declining more contracted freight in favor of higher-paying opportunities elsewhere. As more freight shifts into the spot market, pricing pressure continues to build.

At the same time, freight volumes remain strong. Demand is increasing while available capacity remains constrained, preventing rates from resetting quickly and keeping market conditions firm heading into mid-June.

Areas to Watch

Strategic Considerations

Market Overview

What This Means for the Market

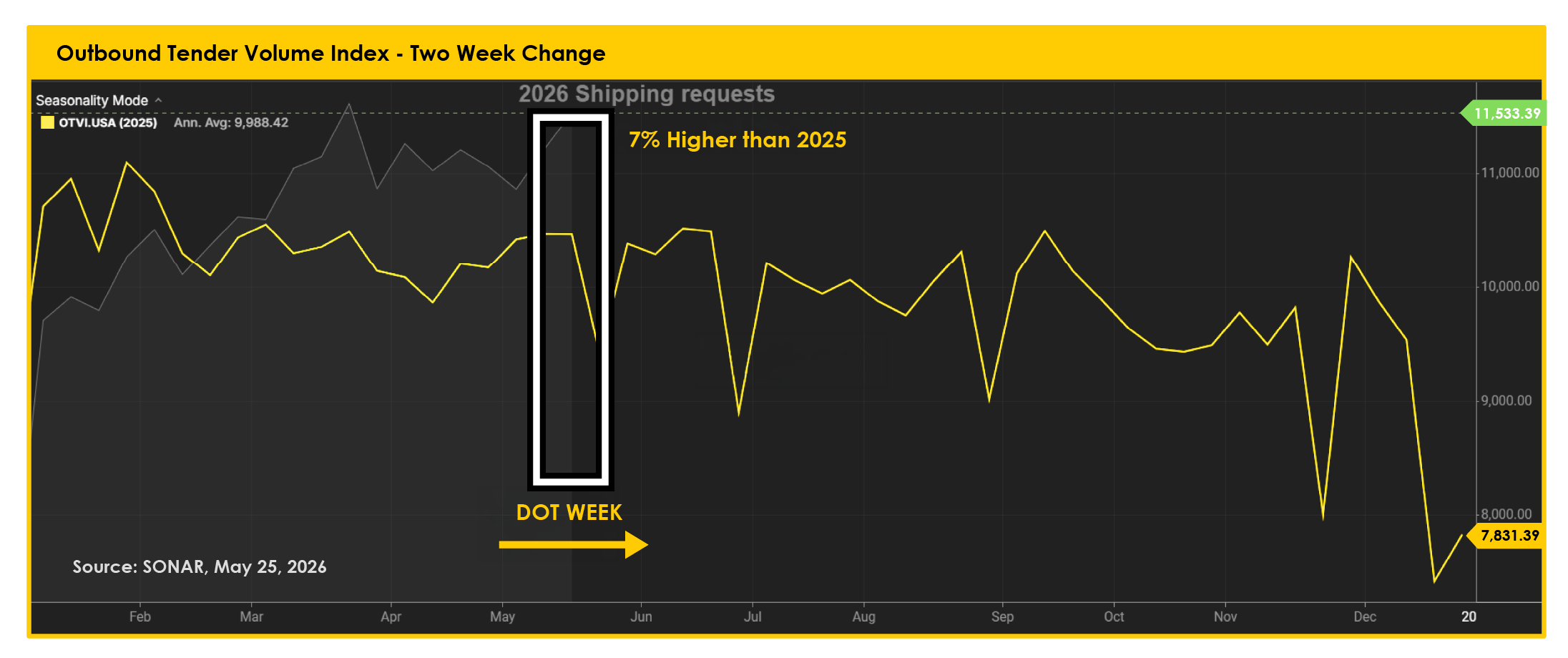

The market moved from tight to tighter over the past two weeks. What we are seeing now is the combined effect of DOT Week, summer freight activity, and continued fuel-driven pricing pressure.

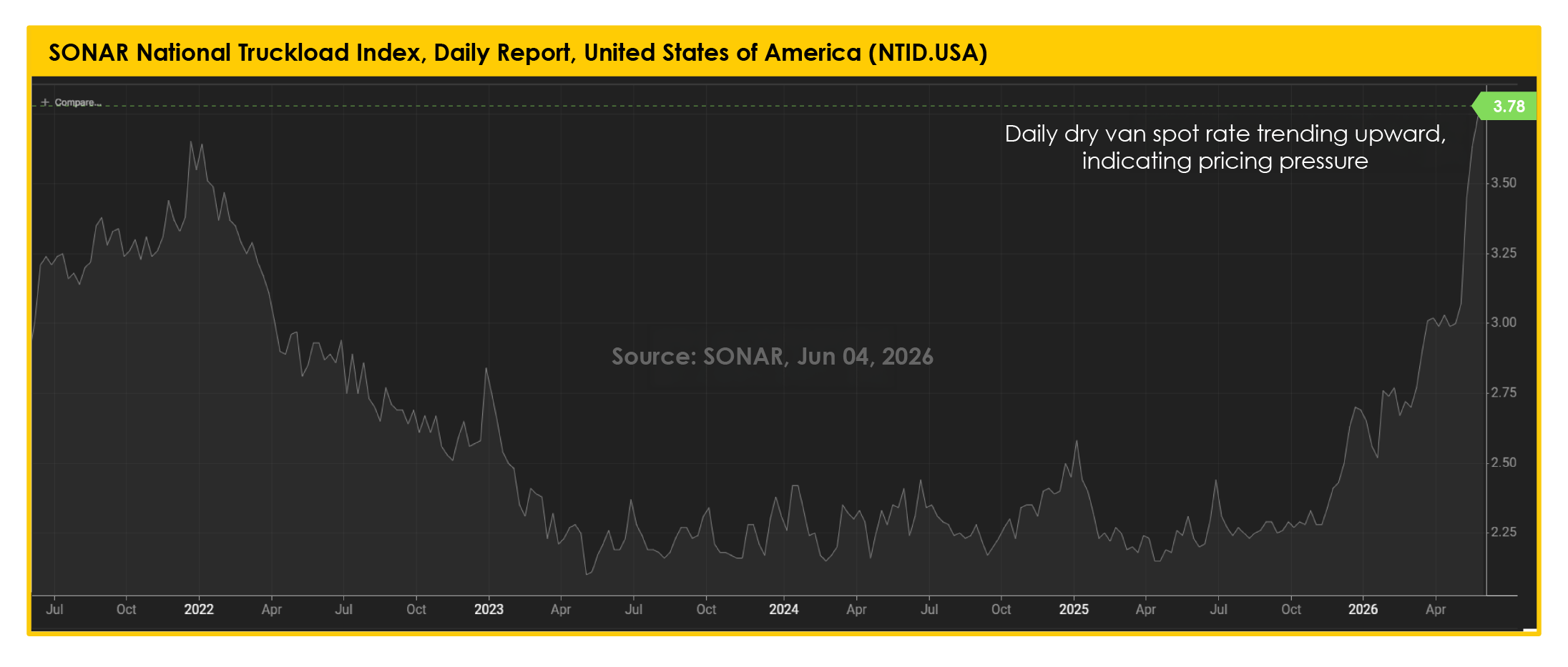

DOT Week was expected to impact capacity, and it did. Fewer trucks were available, carriers became more selective, and spot rates jumped more than 10% week over week while rejection rates moved above 15%.

What stands out now is that rates are not quickly backing down after DOT Week. Instead, they are remaining elevated and continuing to climb. With Memorial Day adding another capacity disruption, the market could move toward some of the highest spot rates seen in recent years.

Spot linehaul rates temporarily moved above contract linehaul rates for the first time since 2022. In simple terms, last-minute freight became more expensive than planned contract freight. That is usually a strong signal that the market is tightening quickly.

Shipping activity remains healthy, but truck availability is becoming increasingly constrained. DOT Week temporarily pulled capacity out of the market while freight demand continued moving higher. When more loads compete for fewer trucks, rates rise quickly.

With Memorial Day, produce season, and summer freight activity ahead, capacity could remain tight over the coming weeks.

Areas to Watch

Strategic Considerations

Market Overview

What This Means for the Market

The market is not loosening. Instead, conditions appear to be stabilizing before the next upward move.

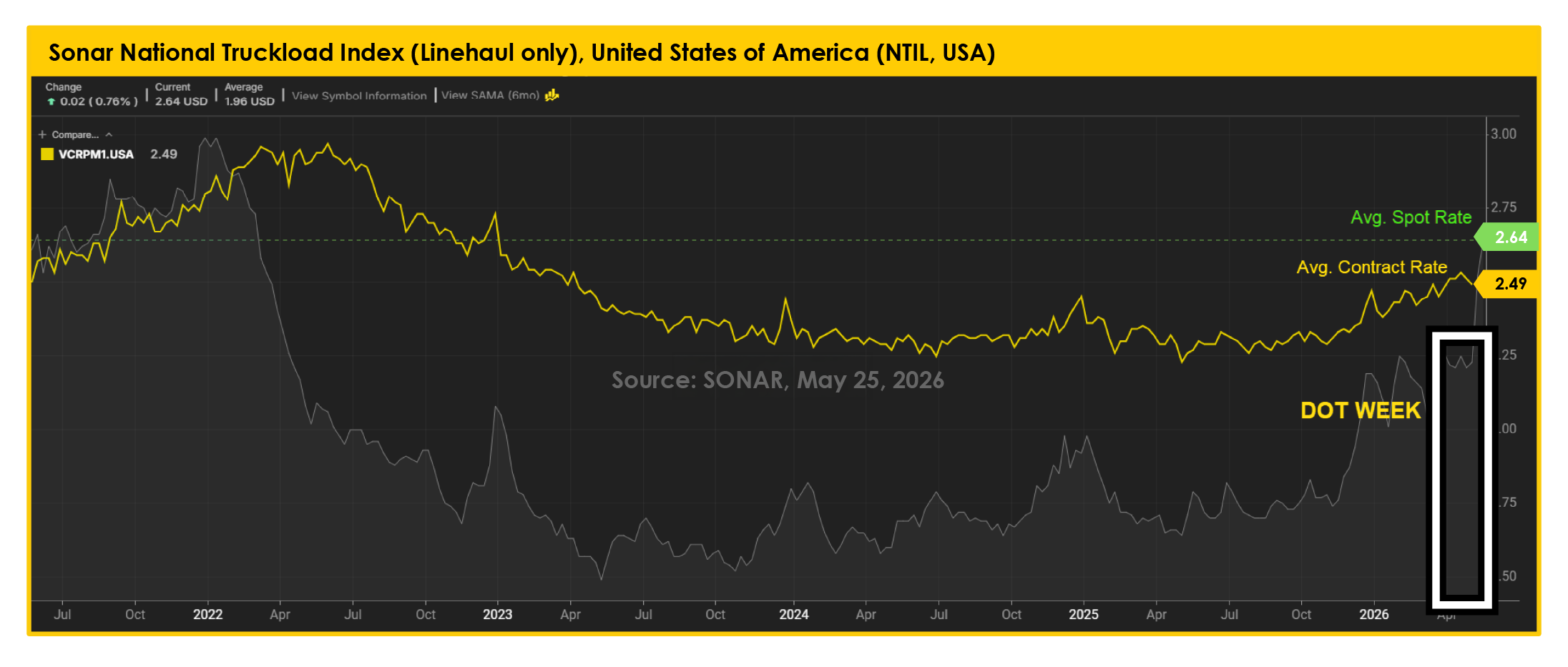

Even with a slight dip in shipping volumes, rejection rates increased and spot rates held firm around the $3.00 mark. That combination matters because it shows that capacity remains limited, preventing any meaningful rate relief.

At the same time, contract rates continue to rise as carriers decline freight at previously agreed pricing. As more freight shifts into the spot market, higher pricing continues to reinforce overall transportation cost pressure. This is no longer a short term spike. It reflects a broader increase in the underlying cost of moving freight.

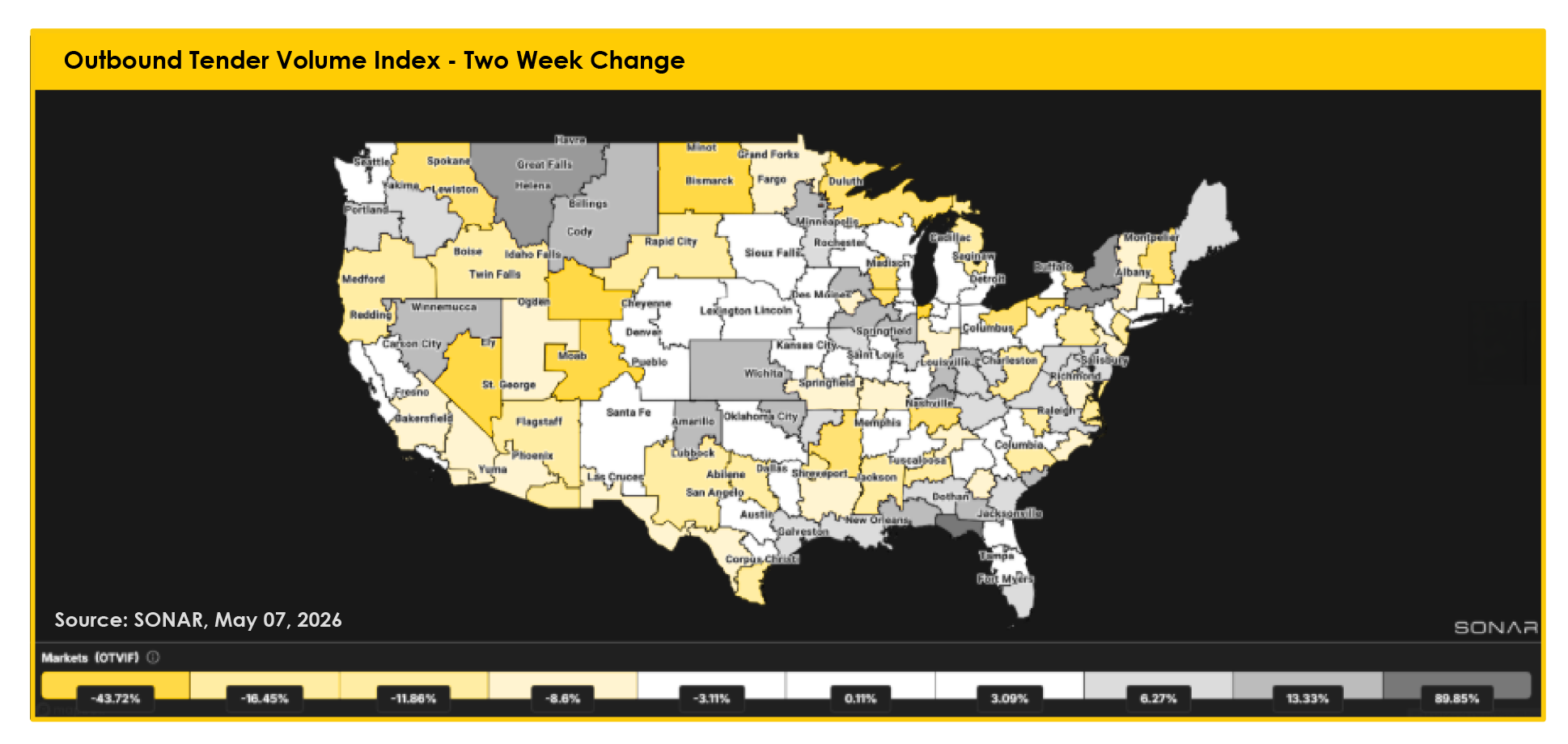

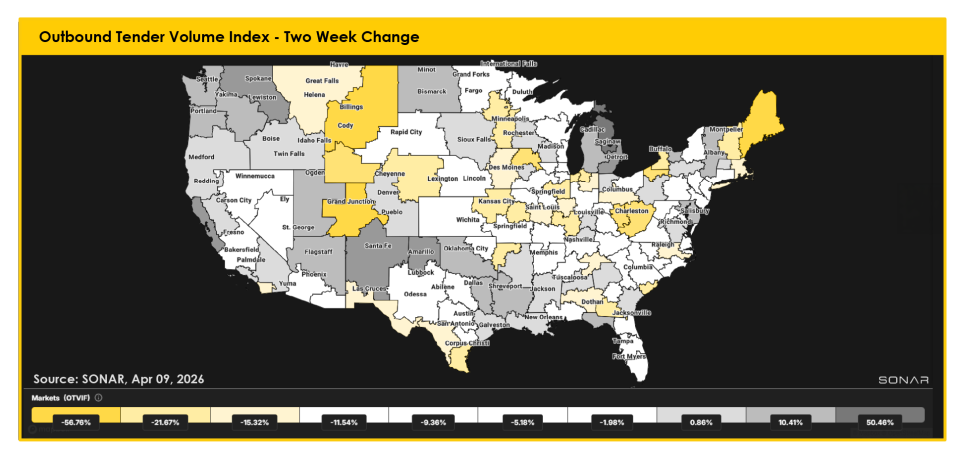

Freight demand also remains uneven across the country. Some markets are softening while others continue to tighten. Produce season is adding additional pressure across key lanes, as more trucks are pulled into produce heavy regions, reducing available capacity for other freight.

With DOT Week and Memorial Day approaching, the market has multiple near term catalysts that could tighten conditions even further.

For shippers, this means that small dips in volume should not be interpreted as rate relief. The market remains expensive, capacity remains selective, and pricing volatility could increase in the coming weeks.

Areas to Watch

Strategic Considerations

Market Overview

What This Means for the Market

The market is showing some early signs of easing, but not enough to shift pricing.

Even with a slight drop in volumes and fewer rejected loads, rates have not moved down. This reinforces that pricing is not being driven by fuel alone. The underlying cost of moving freight remains high, and carriers continue to hold the advantage.

Data trends support this. While rejection rates dipped slightly, they remain elevated overall. At the same time, both spot and contract rates are holding at multi-year highs, indicating that base freight pricing is sustaining current cost levels, not just fuel.

For shippers, this means that even when demand softens week to week, costs are not declining alongside it. Fuel is adding pressure, but it is not the primary reason rates remain elevated.

Areas to Watch

Strategic Considerations

Market Overview

What This Means for the Market

The market is heating up again. Demand is rising, carriers are rejecting more loads, and spot rates are climbing together – a clear sign that conditions are tightening, not easing. Carriers hold a leverage of choosing, making some contracted shipments harder to cover and increasing the risk of higher spot costs. At the same time, fuel is pushing up total shipping costs, not just surcharges, bringing spot and contract rates closer together. The takeaway: costs are rising, and opportunities to lock in lower rates are starting to narrow.

Areas to Watch

Strategic Considerations